PDFChef by Movavi

Everything you need from PDF software!

* The trial version of PDFChef by Movavi has the following restrictions: 7-day trial period, watermark on the output PDF.

How to Create a Profit and Loss Statement

Download a form filler by Movavi.

Open a fillable profit and loss statement and complete it.

Save the finished profit and loss statement.

Print the document or send it by email.

By clicking the download button, you're downloading a trial version of the program.*

What is a profit and loss statement?

A profit and loss statement, also known as an income statement or revenue statement, is a financial statement that shows a company's revenues and expenses (profits and losses) over the course of a set period of time.

There are various other terms that can be used to describe this document. It may be referred to as a statement of profit and loss, a statement of operations, an earning statement, an expense statement, or a statement of financial results. So if you worry about what is the difference in profit and loss vs. income statement, there's no need for concern, as they're both the same thing.

The purpose of this statement is to show how the net income of a company after the expenses are deducted from the revenues. It's essentially a simple way of showing how much money a company is making or losing, based on how much it generates and spends.

Every public company is obliged to share its profit and loss statements on a quarterly and annual basis. It can be a valuable document for learning more about how a company is performing financially and where changes might be able to be made to increase profits.

It's similar to a balance sheet in some ways, but it's important not to confuse the two. Balance sheets only show a company's financial balances at a singular moment in time, whereas profit and loss statements show net income over the course of a period of time, usually a fiscal quarter or fiscal year.

If you're looking into how to create a profit and loss statement, a good option is to make use of a simple PDF template. This free template basically gives you a blank canvas with the general structure and layout of the form already prepared for you, so all you have to do is fill in the necessary information to finalize your statement.

Structure of a profit and loss statement

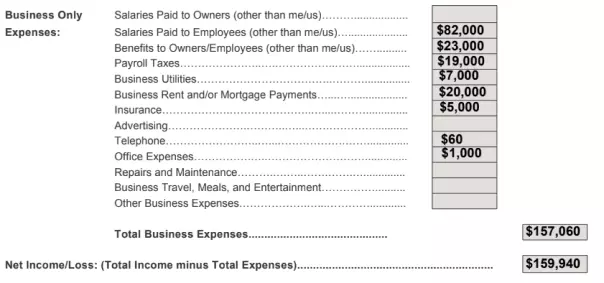

Profit and loss statements follow the same basic format, split up into five main sections: income, cost of goods sold, expenses, other income and expenses, and net income.

Each of the first four sections is structured in the same way, with individual lines for each income and expense category and a value showing how much your company earned or spent in that particular category.

The statement usually begins with the income or "top line" of the business, which covers the amount of money the company has made over the course of a quarter or year.

The various other sections are then filled out underneath that, such as the cost of the various goods your company sells and all additional expenses, like operating costs, taxes, interest, the cost of supplies and equipment, admin expenses, and so on.

The costs of the expenses are then subtracted from the top line, resulting in the "bottom line" or net income cost, also known as profit or earnings, which appears near the bottom of the statement.

Why might you need a profit and loss statement?

Well, it's one of the most fundamental documents to show if your business is profitable, as well as demonstrating whether or not your current business plan is viable and able to be sustained over the long term.

It can also help you spot ways to change your plan to raise profits and lower expenses. For example, by itemizing all expenses on a profit and loss statement, you might notice certain areas in which you are spending more than necessary, so these statements can be really helpful for companies that want to make alterations to their business strategies and develop their plans as they move forward.

These statements can provide plenty of other valuable insight too. They can show, for example, where most of your revenue comes from, allowing you to identify revenue streams that are particularly important for your brand and highlight those that aren't performing as well.

Plus, you can compare profit and loss statements to other key business statements like balance sheets and cash flow statements to get a big picture of how your business is performing, growing, and changing over time. So it's fair to say that these statements hold a lot of importance for the average company.

What don't these statements show?

When it comes to how to read profit and loss statements, it's important to be aware that they don't necessarily give you the full view of a business’s standing and value, as there are certain items that don't appear on a typical example statement.

An income statement will not, for example, show any assets owned by the company, nor will it include liabilities or equity. So it won't cover things like equipment your company owns, security deposits you might have paid in the past, credit card payments, loan repayments, money that has been lent to others, and so on.

For this reason, along with others, you can't rely solely on a profit and loss statement to get a full and clear picture of a company's position. They're great for providing an indicator of how a company is performing financially in the current year to date, but other monthly and long-term financial documents need to be taken into account as well.

Do you have to make a profit and loss statement?

Public companies are legally obligated to prepare these kinds of statements and have to file them according to strict regulations. Private companies, meanwhile, are not usually obligated to prepare any P&L statements, and some choose not to do so.

However, as explained above, these kinds of statements can provide a lot of valuable insight into how a business is running, as well as being useful when developing a business strategy or plan for the company to grow in the future.

So it is often recommended to make profit and loss statements, especially for small businesses and startups in the early months of their operation, as the information these statements provide can be valuable later on.

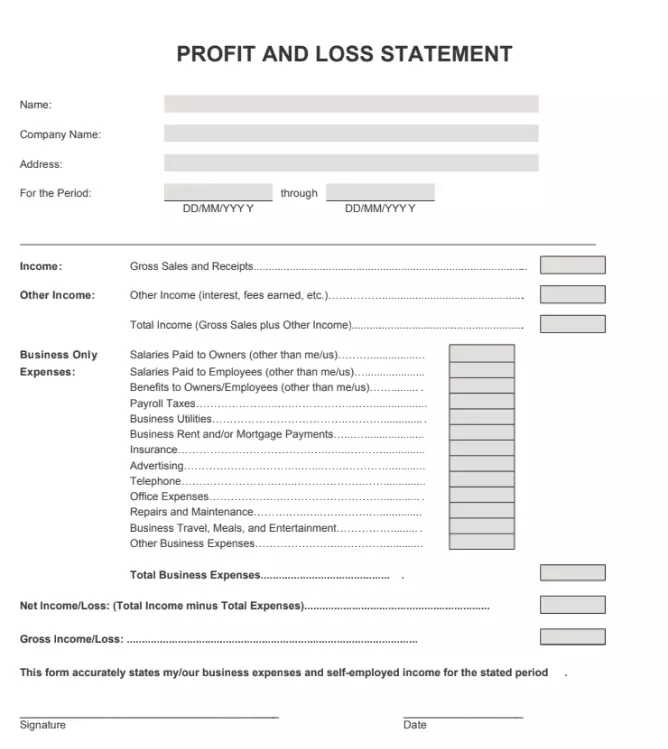

Profit and loss statement sample

Below, we'll go over a simple sample of a profit and loss form, allowing you to gain a better understanding of how to make one of these statements for a small business of your own or for self-employed people.

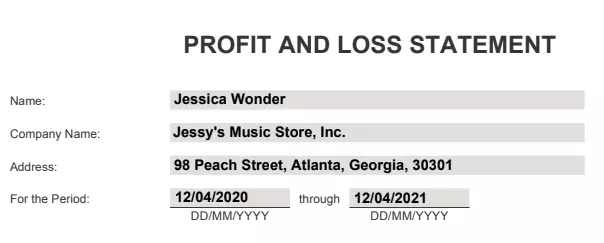

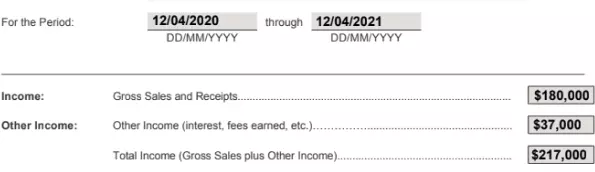

1. At the top of the profit and loss statement, you can enter your company's name and the current date on which the statement is being made. You can also choose a time period for which the statement will apply, which might be the previous year or the previous quarter, or you might even want to make a monthly profit and loss statement. This can be entered near the top of the page.

Disclaimer: The templates here are provided for reference only and you should always talk to a professional for all legal matters.

2. Next, it's time to focus on the revenue, which is the first major section of any P&L statement. Here, you should input your business' income details from sales and services you have provided. You should be able to make use of your current account balances to work out your total revenue over a set period of time, and you can enter the value in the Total Revenue section.

3. The next step is to focus on calculating the cost of the goods you sold, if applicable. So if you have a company selling accessories, you need to think about the supply costs for those accessories and how much you paid to get them in the first place, including any materials and labor. If you don't sell goods, but instead sell services, you'll still need to work out a value for this section, focusing on the amount spent on labor and employee salaries to provide the services.

4. Once you've worked out the total cost of goods sold or services provided, you can subtract this from your revenue to work out your company's gross profit or loss and enter this value in the corresponding line on the statement.

5. Then you can move on to your operating expenses. This includes everything from equipment, utilities, rent, travel, payroll, and so on. Enter each value in its own line to separate them all, and add them all up to attain a total operating expenses value. Take this value away from your gross profit value to get your company's operating profit or loss value.

Disclaimer: The templates here are provided for reference only and you should always talk to a professional for all legal matters.

6. Next, we have the other income and expenses section. Here, you can enter any additional income, like interest income from investments, as well as additional expenses like taxes and amortization. Work out the difference between your operating profit/loss value and all the additional profits and expenses to gain your net profit/loss value, which you can enter at the bottom of the statement.

Disclaimer: The templates here are provided for reference only and you should always talk to a professional for all legal matters.

PDFChef by Movavi

* The trial version of PDFChef by Movavi has the following restrictions: 7-day trial period, watermark on the output PDF.

Have questions?

Join us for discounts, editing tips, and content ideas

1.5M+ users already subscribed to our newsletter